- Bitcoin has underperformed the high expectations post-halving

- Large global liquidity supply increases have been strong upside catalysts for Bitcoin

- Policymakers have little reason at present to conduct such stimulative policies

- Bitcoin is likely to continue to trade in its range with interim volatility

- Consider writing cash-secured puts or using covered calls to reduce outsized Bitcoin positions

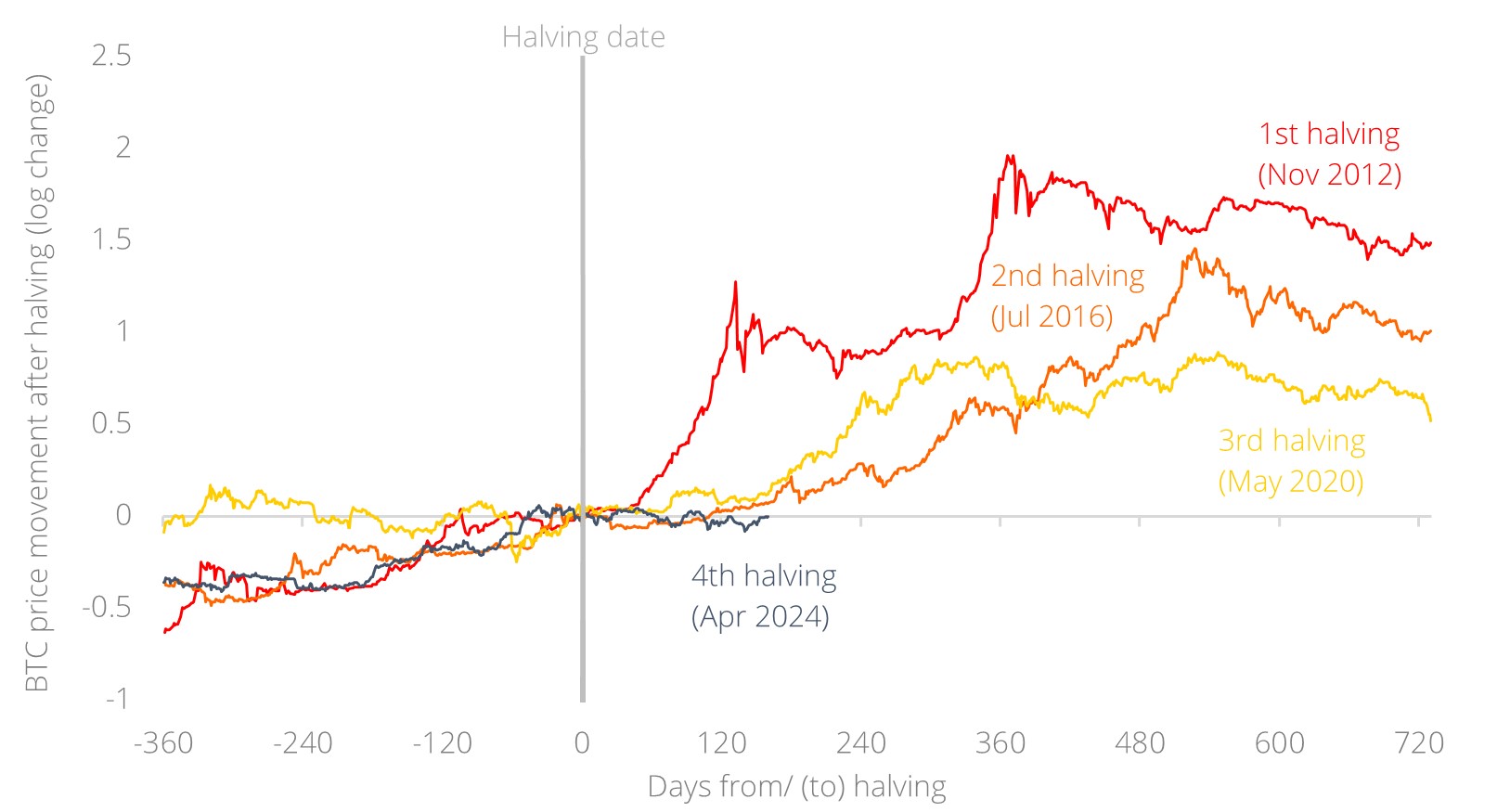

Are we there yet? As far as expectations go, this current Bitcoin halving cycle has disappointed many enthusiasts; one would think that a halving of supply and regulatory approval of spot ETFs would be a one-way ticket to the multi-bagger moon. Prices however, have struggled to break above the USD73k mark set in March this year, just a month prior to the halving in April. Compared to its own short history of halving events, this fourth cycle has seen the most muted movement thus far compared to its predecessors (Figure 1).

Figure 1: Fourth halving has yet to live up to expectations set by its predecessors

Source: Bloomberg, DBS

Feeling the pulse. There is a useful sentiment gauge that quite adequately explains the low directional conviction that the market has fluctuated in since the halving event. It employs a measure known as the “Realised market capitalisation” – the average price at which Bitcoin was last transacted on-chain (Coinmetrics), multiplied by the total circulating supply – essentially an estimate of the average entry price of the cohort of Bitcoin holders. Comparing this to the actual market capitalisation – specifically using the market value/realised value (MVRV) ratio, this gives an estimate of how “in the money” the average Bitcoin holder is.

Glass is half full/empty. At present, the actual market cap lies handily above the realised market cap, suggesting that Bitcoin holders on aggregate remain well in the money. Looking at the MVRV ratio however, the current ratio of c.2x is still far below the 3-4x multiples that were obtained in the previous two halving cycles. Therefore, the market presently sits in this conundrum where (a) holders are unlikely to add aggressively to their positions because valuations are not particularly cheap, but (b) neither are they willing to sell because the perceived upside has not been realised (yet).

In our CIO Perspectives – Beyond the Bitcoin Halving Cycle (4 Jun 2024), we highlighted that we would “likely see Bitcoin fluctuate sideways in a range till the next catalyst”, and that “the next catalyst would likely be centered around monetary policy easing in some form”. While the outsized 50 bps US Fed cut and People’s Bank of China’s reductions in Reserve Requirement Ratios (RRR) and adjustments to policy and mortgage rates in September do represent a shift in the global monetary policy direction, these only represent a change in the price of money, and relying on multiplier effects to indirectly increase the supply of money. We have observed Bitcoin performing much better under actions that directly increase the supply of money instead – such as QE or large deficit spending; stimuli that have yet to come to market en force.

Bitcoin has strong correlations with global liquidity. In fact, in no other asset do we see liquidity being such a positive driver for prices as it does with Bitcoin. There have been many representations of how ample global liquidity conditions have amplified the returns on risk assets, such as comparisons of Global M2 against the S&P 500 index (Figure 3, right); which is perhaps why investors still hang onto the words of central bankers with baited breath till this day. More than the S&P 500 however, is the fact that Bitcoin has one of the highest directional alignments with global liquidity – with positive 12-month rolling correlations in c.88% of the time since 2011. It’s also uncanny to consider that the periods where such correlations break down occur under idiosyncratic risk events (crypto exchange collapses, rug-pulls etc.) generally unrelated to liquidity conditions.

Moving everywhere, going nowhere. Seeing as Bitcoin is likely to range trade due to (a) the MVRV ratio being neither cheap nor expensive, and (b) markets navigating the balance between policy support and slower growth, we believe that the conditions are likely to precipitate interim volatility, which makes volatility-selling structures an interesting proposition while the market awaits a larger liquidity catalyst.

How does one capitalise on uncertainty? Depending on one’s risk appetite, monetising volatility could come in two forms:

1. Writing cash-secured puts. For the bullish investor who feels that they “missed the boat” when Bitcoin first began its ascent early this year, writing puts is a good strategy to monetise premiums while awaiting to buy Bitcoin at a lower strike price.

2. Writing covered calls. For the investor that wishes to decumulate an outsized position in Bitcoin, writing call options is a good strategy to generate income while setting an acceptable profit-taking strike price to reduce overall holdings.

Making lemonade with lemons. The most common refrain with Bitcoin (and other cryptocurrencies in general) is its stomach-churning volatility that far exceeds those of other risk assets. Option structures allow investors to turn such drawbacks to advantages. In periods of high uncertainty, volatility can be capitalised for the benefit of investors through options structures, harvesting premiums on the side while waiting for a clearer trend to emerge for taking more directional bets.

Download the PDF to read the full report.

Topic

This information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

The information contained in this article has been obtained from sources believed to be reliable, but DBS makes no representation or warranty as to its adequacy, completeness, accuracy or timeliness for any particular purpose.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.

Please refer to the Additional Terms and Conditions Governing Digital Tokens for DBS Treasures Customers for more specific risk disclosures on trading of digital tokens.

This information does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or enter into any transaction. It does not have regard to your specific investment objectives, financial situation or particular needs. It is not intended to provide, and should not be relied upon for accounting, legal or tax advice.

Cryptocurrency trading is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. Before you decide to purchase an investment product, you should read all the relevant documents and carefully assess if it is suitable for you. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single asset type.

Trading in Cryptocurrencies or the instrument (“Instrument”), such as ETF, referencing or with underlying as Cryptocurrencies ("Crypto-Products”), such as Bitcoin ETFs, is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. By trading in Crypto-Products, you are exposed to the risks of both the Instrument and the Cryptocurrencies. Further, Crypto-Products listed on overseas exchanges may not be regulated in Singapore, and are subject to the laws and regulations of the jurisdiction it is listed in. Before you decide to buy or sell Cryptocurrencies or Crypto-Products, you should read all the relevant documents and carefully assess if it is suitable for you and/or seek advice from a financial adviser regarding its suitability. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single asset type.

To the extent permitted by law, DBS accepts no liability whatsoever for any direct, indirect or consequential losses or damages arising from or in connection with the use or reliance of this email or its contents. If this information has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses.

Please refer to Terms and Conditions governing your banking relationship with DBS for more specific risk disclosures on the Instrument (such as ETFs under Funds) and Digital Tokens.

This information is provided to you as an “Accredited Investor” (defined under the Securities and Futures Act of Singapore and the Securities and Futures (Classes of Investors) Regulations 2018) for your private use only. It is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, and may not be passed on or disclosed to any person nor copied or reproduced in any manner.

DBS (Company Registration. No. 196800306E) is an Exempt Financial Adviser as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore (the "MAS")