Related Insights

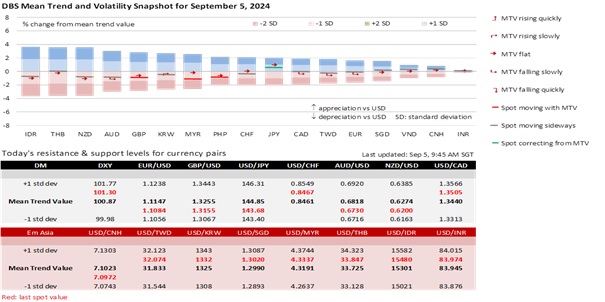

The DXY Index’s five-day recovery stalled, depreciating by 0.6% to 101.26. The greenback’s overall weakness, driven by Fed cut expectations, was most evident in the CAD, which appreciated by 0.3% to 1.3506 per USD. This appreciation occurred despite the Bank of Canada signalling further rate cuts after delivering its third 25 bps reduction to 4.25%. Meanwhile, the CHF is on the verge of reclaiming all of this year’s losses, prompting the Swiss National Bank to reinforce its dovish stance ahead of a third rate cut expected on September 26. The JPY strengthened further, appreciating by 1.2%, adding to Tuesday’s 1% rebound on the Bank of Japan’s commitment to keep hiking rates. USD/JPY ended at 143.74 overnight, its lowest close since January 3. A break below 143.50 could push the currency pair to retest the intra-day low of 141.70 on August 5. As the USD continues to lose ground against the JPY, this trend may extend to other currencies in the DXY basket. The GBP and EUR have already reversed this year’s losses into gains around mid-August.

The US Treasury yield curve sloped positively for the first time since July 2022. The spread between the 10Y and 2Y yields closed at 2.4 bps, following a 10.9 bps decline in the 2Y yield to 3.754% and a 7.6 bps drop in the 10Y yield to 3.755%. The July US JOLTS jobs openings report showed the weakest reading since January 2021, with openings falling to 7673k, well below the 8100k consensus. June’s figure was also revised to 7910k from its previously estimated 8184k. The data is significant because the Fed has been closely monitoring the Beveridge Curve, which links rising unemployment rates to declining job openings. Today’s ADP Employment report and initial jobless claims will be closely watched for tomorrow’s nonfarm payrolls and unemployment rate data.

The Fed’s Beige Book supported Fed Chair Jerome Powell’s “the time has come” call to reduce interest rates. The number of districts reporting flat or declining economic activity increased to 9 in the current period from 5 in the previous period. Only 3 districts reported a slight increase in activity. Given the uncertainties over demand and the economic outlook, employers became more selective with their hires and were less likely to expand their workforces amid expectations for price and cost pressures to stabilize or ease further in the coming months. Although the employment levels were flat to up slightly in recent weeks, job seekers faced increasing difficulties and longer times to secure a job. Hence, markets will likely scrutinize today’s ISM Services PMI report through the same lens.

Quote of the day

”Companies don’t give job security. Only satisfied customers do.”

Jack Welch

September 5 in history

Canada put its first gold bullion coin on sale in 1979.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.