Related Insights

- DEER: Watching JPY and GBP risks 09 Jun 2026

- India markets: Details on BOP-supportive measures, pressure to ease 09 Jun 2026

- USD Rates: Inflation watch 09 Jun 2026

There are two key takeaways from the Fed minutes released overnight. First, the minutes offered a more cautious take on easing. Many participants that it is “complicated” to assess the degree of restrictiveness on current monetary policy settings. In particular, the appropriate neutral rate is uncertain and may well be higher than what the Fed pencilled in for September (2.9%). From the market’s perspective, this is not new. Given resilient US data and upside growth / inflation risks, the market is barely pricing in three more cuts by the end of 2025, taking the FFR to 4%. In any case, we still think the Fed would cut in December, but could well signal an even slower pace of easing going forward.

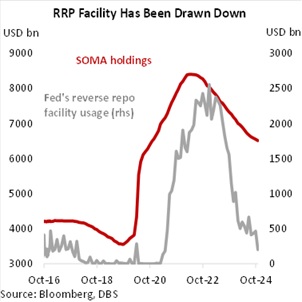

Second, the Fed hinted on a “technical” adjustment in the RRP rate. Currently, the RRP rate stands at 4.55bps, 5bps higher than the FFR lower bound. The Fed is mulling aligning the RRP to the FFR floor, which would imply a 5bps rate cut. Given that the Fed is considering such an option, it may mean that such a change is imminent (probably December’s FOMC meeting). Funds placed at the RRP facility has declined steadily from close to USD 2.5tn to around USD 148bn currently as QT progresses. If the tweak occurs, the remaining funds could flow out into other short-term instruments, lowering short-term USD rates in general. That said, this looks to be a one-off adjustment on rate levels and short-end swap spreads (turn more inverted). The motivations for the Fed could be twofold – to ensure sufficient liquidity to cross the year end and to prepare for the end of QT some time in 2025.

Topic

Explore more

E & S Macro StrategyGENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.

Related Insights

- DEER: Watching JPY and GBP risks 09 Jun 2026

- India markets: Details on BOP-supportive measures, pressure to ease 09 Jun 2026

- USD Rates: Inflation watch 09 Jun 2026

Related Insights

- DEER: Watching JPY and GBP risks 09 Jun 2026

- India markets: Details on BOP-supportive measures, pressure to ease 09 Jun 2026

- USD Rates: Inflation watch 09 Jun 2026